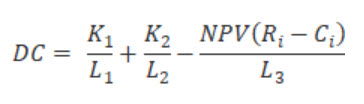

Our 2018 determination and final report on maximum prices to connect, extend or upgrade a service for metropolitan water agencies set out a formula for calculating developer charges:[1]

A key objective of this formula is to ensure that developers pay the full costs of capital works that are for the exclusive benefit of their development, and partially pay the costs of capital works already undertaken that benefit both their development and existing customers of the public water utility. If these cost recovery principles were not in place, then existing customers would end up paying for costs caused by the development.

The formula contains terms K1 and K2 which refer, respectively, to capital charges for pre-1996 and post-1996 assets that will serve the DSP area. Post-1996 assets are those commissioned on or after 1 January 1996, including assets that are not yet commissioned. These capital charges involve an apportionment of capital costs to a DSP. [2] The portion assigned to each DSP will be based on expected utilisation. Utilisation means the number of equivalent tenements (ETs) in the DSP as a proportion of the total number of ETs served by an asset.[3]

The apportionment of capital costs will likely be different for each asset, and will certainly be different for assets of different categories (eg, pre-1996, 1996-present, future). This asset-specific apportionment is illustrated in the template calculation spreadsheet IPART published with its determination in October 2018. (See tabs “Pre-1996 assets”, “Post-1996 commissioned assets” and “Uncommissioned assets”.)

Utilities subject to the 2018 determination should not apply the same apportionment ratio to the different asset categories. We are also publishing an updated template calculation spreadsheet that illustrates this point more clearly by use of an example. (See the corresponding tabs of the new spreadsheet.)

[1] See clause 1(b) of the determination and Box 2.1 of the final report.

[2] Some assets are excluded. For example, those provided for a reason other than growth, servicing other DSP areas, unreasonably oversized, commissioned prior to 1970 or funded by developers and transferred free of charge.

[3] The final report made it clear that capital costs were to be included on an ‘incremental cost’ basis, which means that new customers make an upfront contribution to the costs of existing assets, to the extent that these assets form part of the servicing solution for the new development (see Box 2.2, p 23). This extent will probably differ from asset to asset.