IPART reviews the performance of the market each year to assess how competition is working under section 234A of the National Energy Retail Law (NSW).

Our review of the performance of the market for 2017-18 is our fourth annual monitoring report on the retail electricity market, but our first for retail gas market since gas prices were deregulated on 1 July 2017.

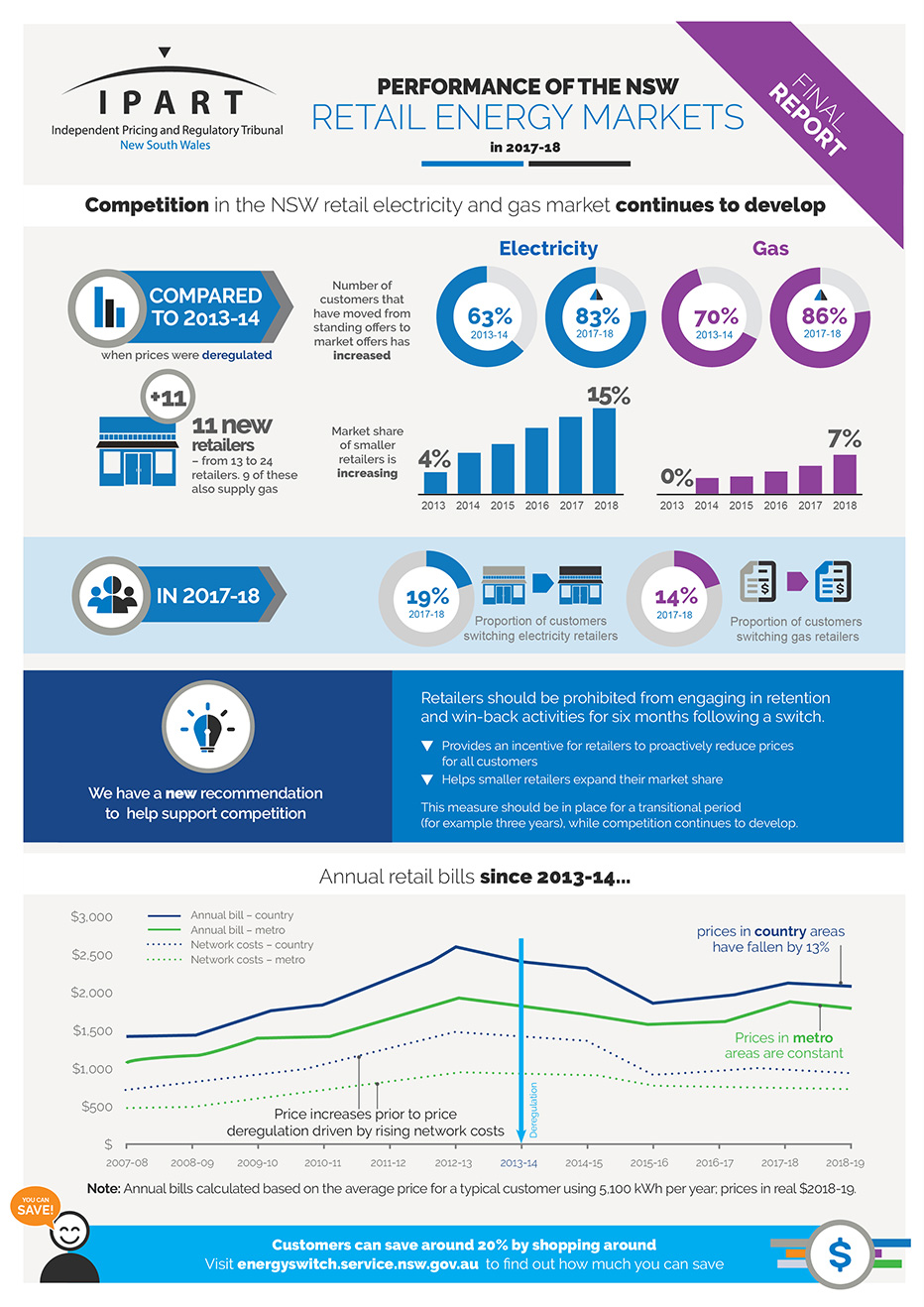

We have found that over the last year:

- Each of the key indicators we use to assess competition in the electricity and gas retail markets were steady or suggested competition increased in 2017-18 compared to the previous year.

- Three new electricity and three new gas retailers entered the markets in the last 18 months, however, the pace at which small retailers has gained market share has been slow.

- Around 19% of electricity and 14% of gas customers switched retailer.

- The changes in electricity and gas prices into 2018-19 reflected efficient costs in a competitive market.

- On average, electricity prices for residential and business customers increased by 0.2% in July 2018 compared to prices in June 2018.

- Gas prices for residential customers in the Jemena network increased by 0.2%, and prices for business customers increased by 1.7%.

- For the country gas networks, gas prices fell on average by around 2% for both residential and business customers.

- Electricity prices are significantly higher than they were 10 years ago, but these increases occurred when prices were still regulated, driven by rising regulated network prices. Since 2013-14 (the last year of price regulation), average electricity bills across NSW have fallen in real terms in line with the net impact of fluctuations in the underlying costs of electricity.

- However, bills for some 17% of customers – those who have not actively engaged in the market and are on ‘standing offers’ – are around 26% higher than the lowest offers in the market. Another 18% of customers are likely to be on market offers paying standing offer prices (because their benefit period has expired).

- Governments and regulators are already implementing a wide range of measures to help customers engage in the market and put pressure on retailers to offer lower prices, and these are having a positive effect.

- The NSW Government has launched NSW Energy Switch to make it easier for customers to find the best prices, and it has placed new obligations on retailers to help rebate customers move to lower market offers.

- Other measures to assist customers include the Energy Made Easy website has recently been upgraded, changes to the AER’s Retail Pricing Information Guidelines, and AEMC rule changes to require retailers to notify customers changes to prices and discounts in advance.

We are recommending a further transitional measure should be implemented to support competition. Retailers should be prohibited from engaging in retention and ‘win-back’ activities for six months after a customer has switched retailers, and this measure should be in place for three years while competition continues to develop. This would help smaller retailers grow their customer base so they can compete more effectively over the longer term. It would also put competitive pressure on the big three retailers to proactively offer their customers cheaper prices.

In our view, the most effective way governments can ensure sustainable retail energy prices in the future is to provide a stable and predictable energy market framework. This stability will encourage new investment in the wholesale market, which is essential to increase supply and replace existing generation as it reaches the end of its asset life.

As part of this review, the NSW Minister for Energy and Utilities asked us to report on whether retailers are delivering acceptable levels of customer communication and service in their delivery of metering services.